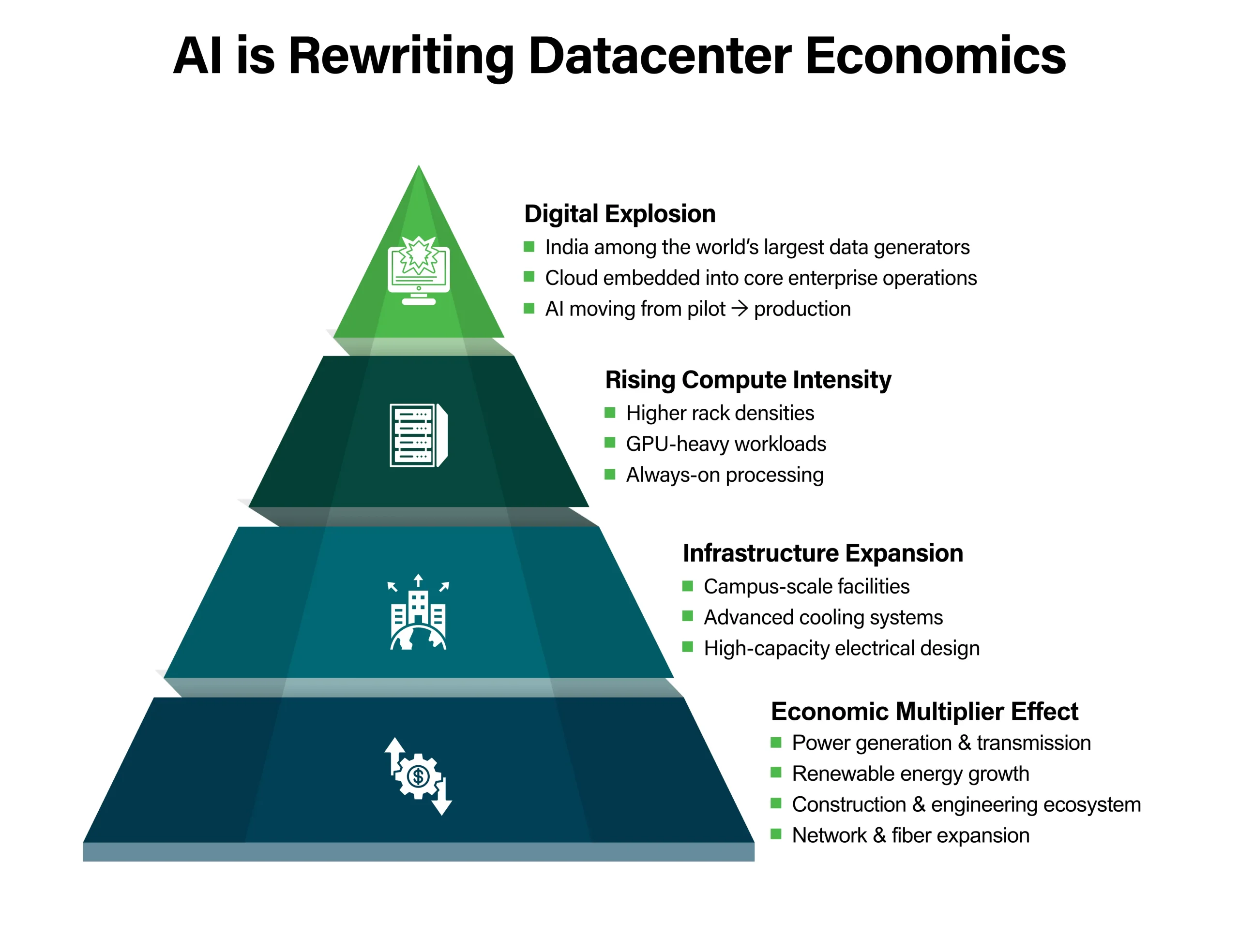

Artificial intelligence is rewriting the economics of digital infrastructure. Globally, hyperscalers are committing hundreds of billions of dollars to AI-ready datacenters, and over the next decade the cumulative investment requirement will run into the trillions. Compute density is rising sharply. Power requirements per rack are increasing. Campus-scale facilities are becoming the norm rather than the exception.

India is emerging as one of the key destinations for this capital, and its share of that opportunity is growing faster than almost any other market.

With expanding cloud adoption, evolving sovereign data frameworks, and rapidly increasing compute intensity across industries, the country’s datacenter sector is entering its most consequential phase of growth. What is unfolding is not a temporary expansion cycle, but a sustained build-out of the digital backbone required to support the next phase of economic development.

From Digital Adoption to Infrastructure Imperative

The drivers of this shift are both domestic and global. India generates one of the largest volumes of digital data in the world and serves a rapidly expanding digital user base. Enterprises across financial services, manufacturing, healthcare, retail, and public services are embedding cloud into core operations rather than treating it as a peripheral IT layer. AI adoption is moving from experimentation into production environments, raising compute intensity and infrastructure complexity.

As digital systems become foundational to economic activity, infrastructure moves from being supportive to being strategic.

At the same time, global capital is rotating toward long-duration infrastructure assets with predictable demand visibility. Digital infrastructure fits squarely within that framework. Unlike short-cycle technology investments, datacenters require sustained capital deployment across land acquisition, civil construction, electrical systems, advanced cooling technologies, network integration, and long-term operations.

They also activate a broader economic ecosystem. Power generation and transmission, renewable energy development, high-voltage equipment manufacturing, construction materials, engineering services, logistics, and connectivity networks all expand alongside hyperscale campuses. At national scale, the cumulative capital required across facilities, energy infrastructure, and supply chains becomes significant.

Current projections suggest India’s datacenter investments will expand several-fold this decade, with cumulative capital commitments already running into tens of billions of dollars. Over the coming decades, as AI adoption deepens and digital infrastructure continues to underpin economic growth, the investment cycle could reach far larger magnitudes.

Budget 2026: Aligning Policy with Long-Horizon Capital

Budget 2026 reinforced India’s long-term commitment to digital infrastructure by extending fiscal certainty for global cloud providers operating from Indian datacenters. For hyperscalers and infrastructure funds making 20- to 25-year deployment decisions, predictability is as important as incentives.

By linking fiscal benefits directly to where infrastructure is physically built and operated, the policy framework signals that digital infrastructure is being treated as national economic infrastructure, not merely a technology sector.

This shift is significant. It reflects a move from export-led digital services growth toward infrastructure-led digital capacity building. It also reduces uncertainty in long-term capital allocation decisions, particularly for global investors evaluating multiple markets for hyperscale expansion.

Recognition of datacenters as critical infrastructure, combined with support for AI, GPU compute, and high-density facilities, aligns policy direction with market demand. When policy clarity, industrial capability, and digital demand move together, capital deployment accelerates.

Budget measures alone do not create growth. But they reinforce momentum when underlying fundamentals are already strong.

Power: The Decisive Variable in the AI Era

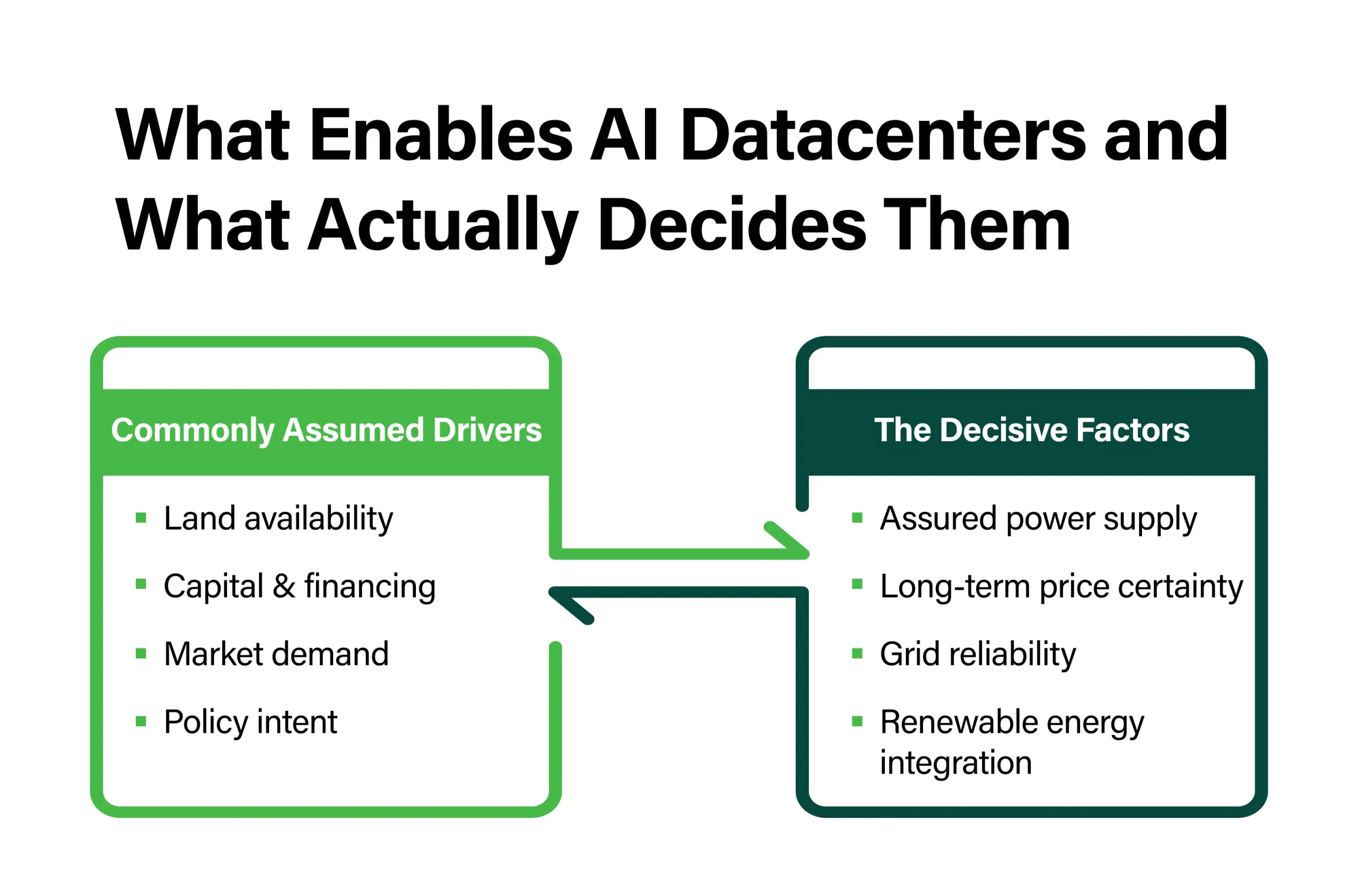

If there is one factor that will determine how quickly India’s datacenter ambition converts into operational capacity, it is power.

Not land. Not demand. Not even financing—which, for well-structured projects, is increasingly available from global infrastructure funds and institutional capital. Power remains the gating variable.

Hyperscale AI facilities require assured electricity supply at predictable prices, sustained over decades. They also require credible renewable integration to meet sustainability commitments and maintain long-term competitiveness. As rack densities increase and cooling architectures evolve, energy planning becomes central to campus design.

States that combine reliable grid access, transmission readiness, long-term pricing clarity, and credible renewable roadmaps will attract disproportionate investment.

India has made meaningful progress. Renewable capacity additions are among the fastest globally. Grid reliability has improved. Open-access frameworks and long-term green power agreements are strengthening supply predictability. Increasingly, state governments recognise that power policy is economic policy.

Execution depth in energy reform will directly influence the pace of hyperscale expansion.

Sovereign Capacity in a Data-Driven Economy

Sovereign cloud considerations further reinforce the need for domestic infrastructure. Across jurisdictions, governments and enterprises are reassessing where critical workloads reside and how data governance frameworks evolve. For a country of India’s scale, digital sovereignty is not merely regulatory; it is strategic.

Hosting critical data and AI workloads domestically enhances resilience, compliance, and long-term economic control over digital systems. As sectors such as financial services, healthcare, defence, and public administration deepen their digital integration, secure and high-availability domestic capacity becomes essential.

The convergence of AI expansion, sovereign requirements, digital demand growth, and long-horizon capital is reshaping how infrastructure decisions are evaluated globally.

From Momentum to Global Leadership

Ambition alone does not guarantee leadership. Execution will determine outcomes.

Land readiness, time-bound approvals, vendor ecosystem depth, engineering capability, supply chain resilience, and coordination between central and state agencies all influence how efficiently capital translates into operational capacity.

India’s progress over the past decade has been tangible. Tier-1 markets continue to scale, while emerging cities are increasingly part of hyperscale evaluation. Engineering maturity has deepened. Institutional capital participation has broadened. Capex-to-opex economics remain favourable relative to many global markets.

Continued focus on transmission timelines, renewable integration, and coordinated permitting will be essential to sustain this momentum.

India’s datacenter story is no longer about catching up. It is about demonstrating, facility by facility and megawatt by megawatt, that this country can execute at the scale the global AI economy demands. For decades, India powered the world’s software and services ecosystem. The infrastructure to support AI platforms, cloud networks, digital commerce, and sovereign digital frameworks is the next frontier, and India has both the opportunity and the obligation to lead it.

The scale is real. The opportunity is real. And India is ready.

Sridhar Pinnapureddy, Founder & CEO, CtrlS Datacenters

A first-generation entrepreneur, Sridhar Pinnapureddy has founded and built to scale several companies in the areas of cloud computing, IT infrastructure, Internet services, green energy, and software development. Under his leadership, CtrlS boasts of creating the world’s largest Rated-4 datacenter footprint with 15 certified operational datacenters and many more in various stages of development, taking the overall capacity to over 1,000 MW.

marketing@ctrls.in

marketing@ctrls.in